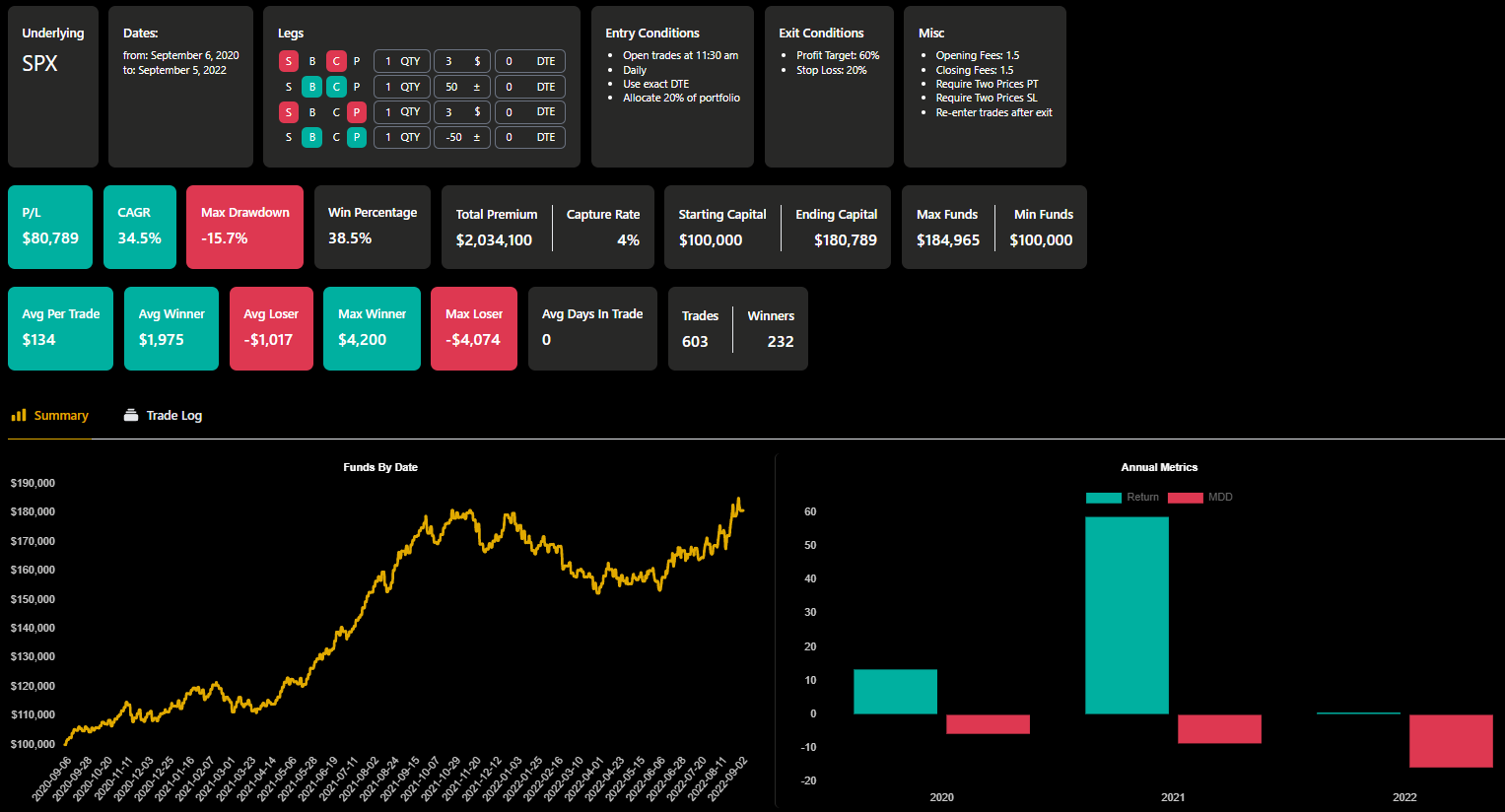

Random Surprise on 0 DTE High Delta Backtest

Didn't really have the intend to write a post but it's interesting enough to share I guess. So I was randomly playing with OptionOmega and I came across this backtest that has such good numbers that I also wanted to keep it for future reference.

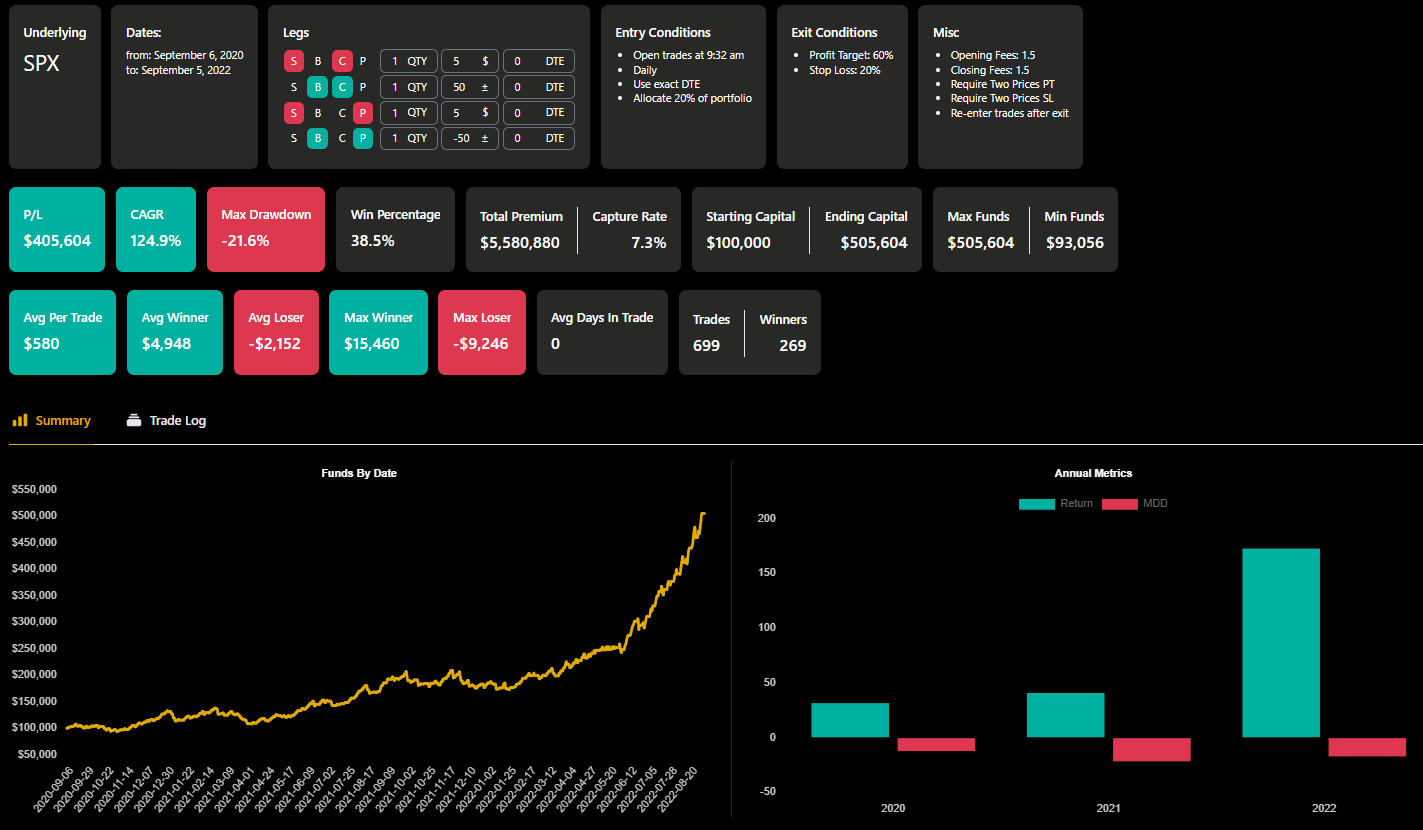

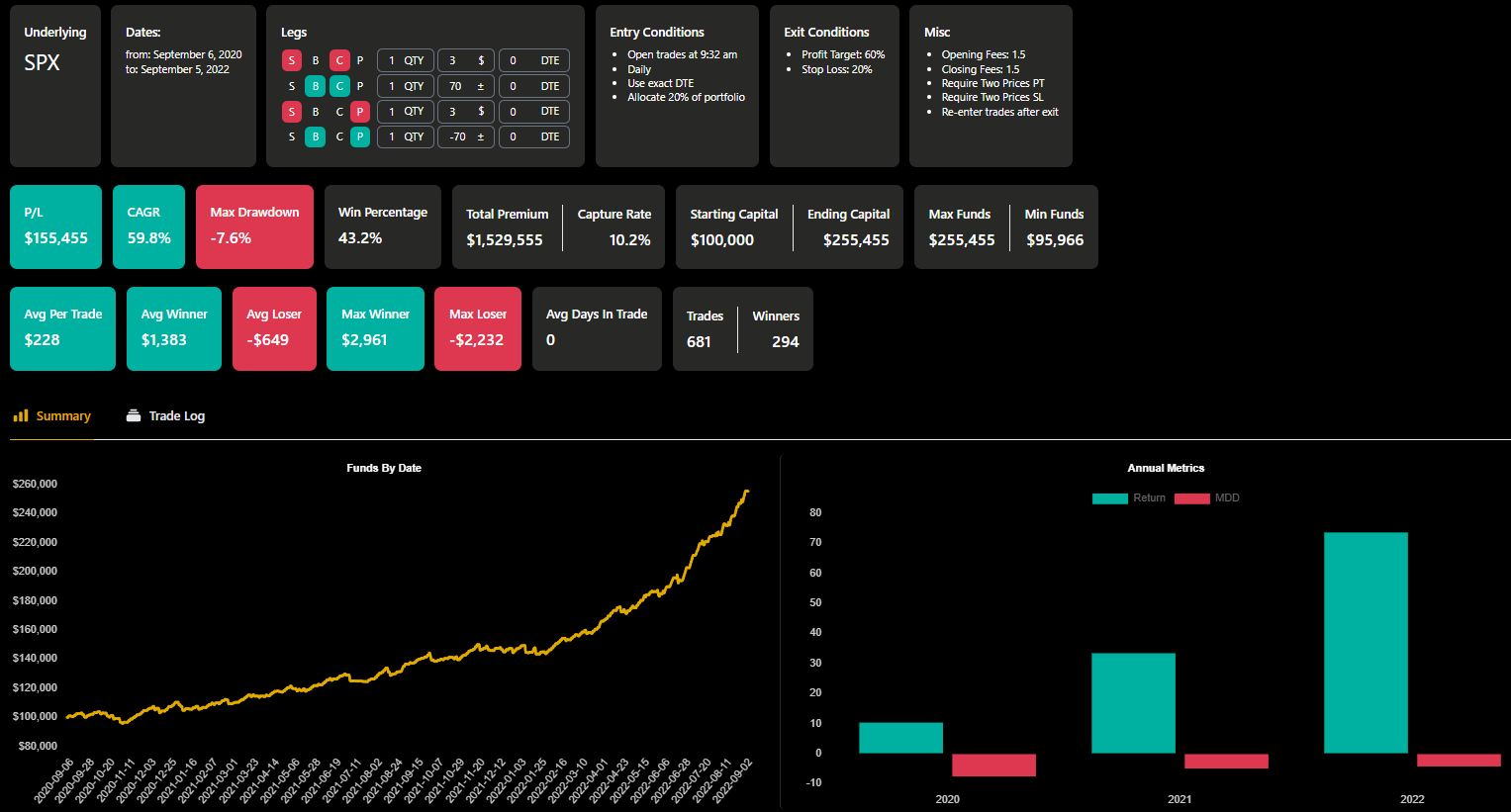

The beauty about OptionOmega is not just the speed (each backtest only takes 15-30secs), it's the screenshot is so self explanatory. Yea, so you read yourself.

I think the key to point out here is the exit conditions of 20% SL and 60% TP. This exit condition forms a 1:3 risk reward ratio. Despite only 38% win rate, it's super high positive expectancy.

Nevertheless, since OO is so fast, it's more than convenient to tweak the configurations here and there to see if there's any differences or how does it affect the performance.

So more screenshots.

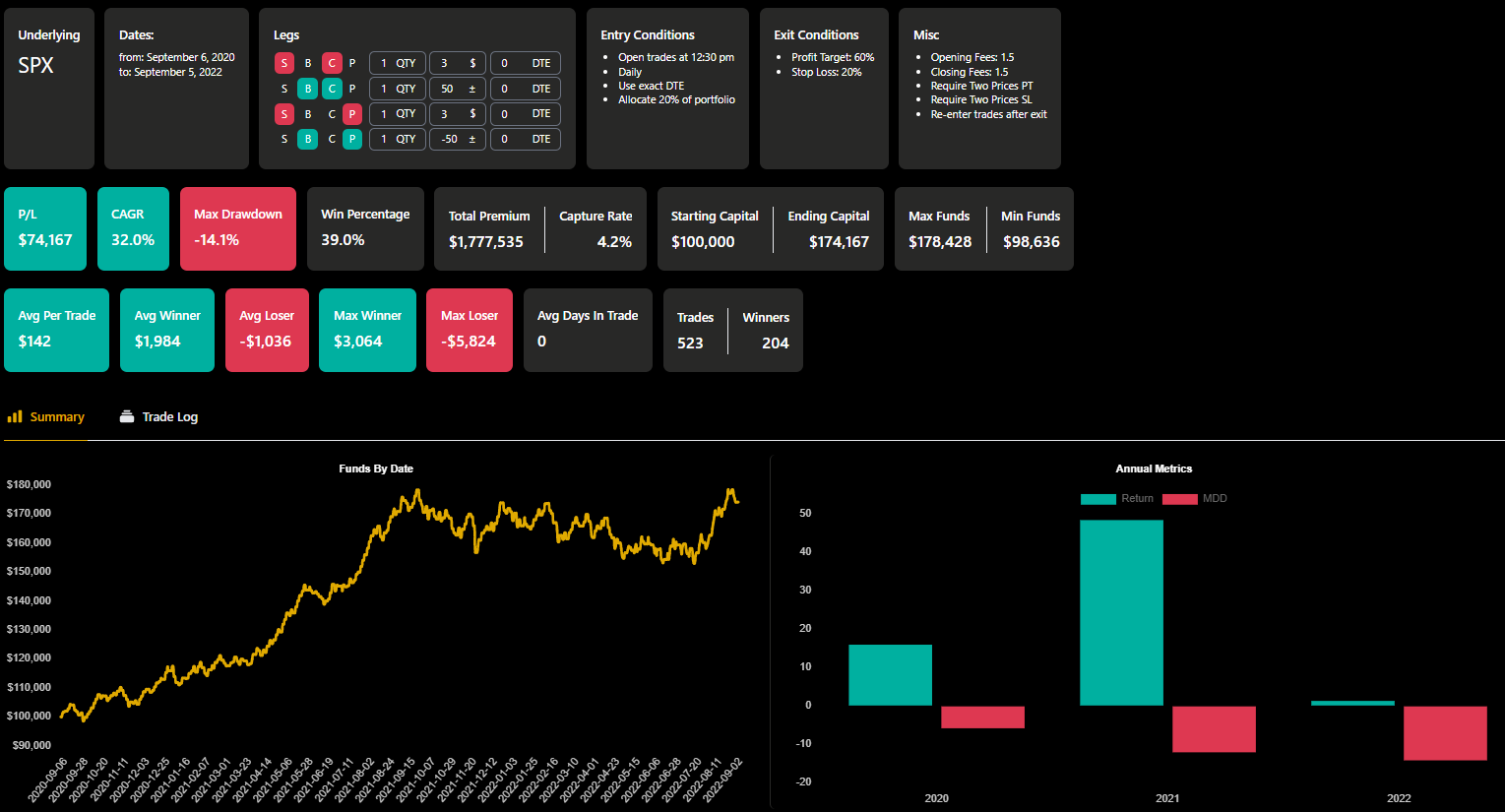

First thing to tweak - Credit Target

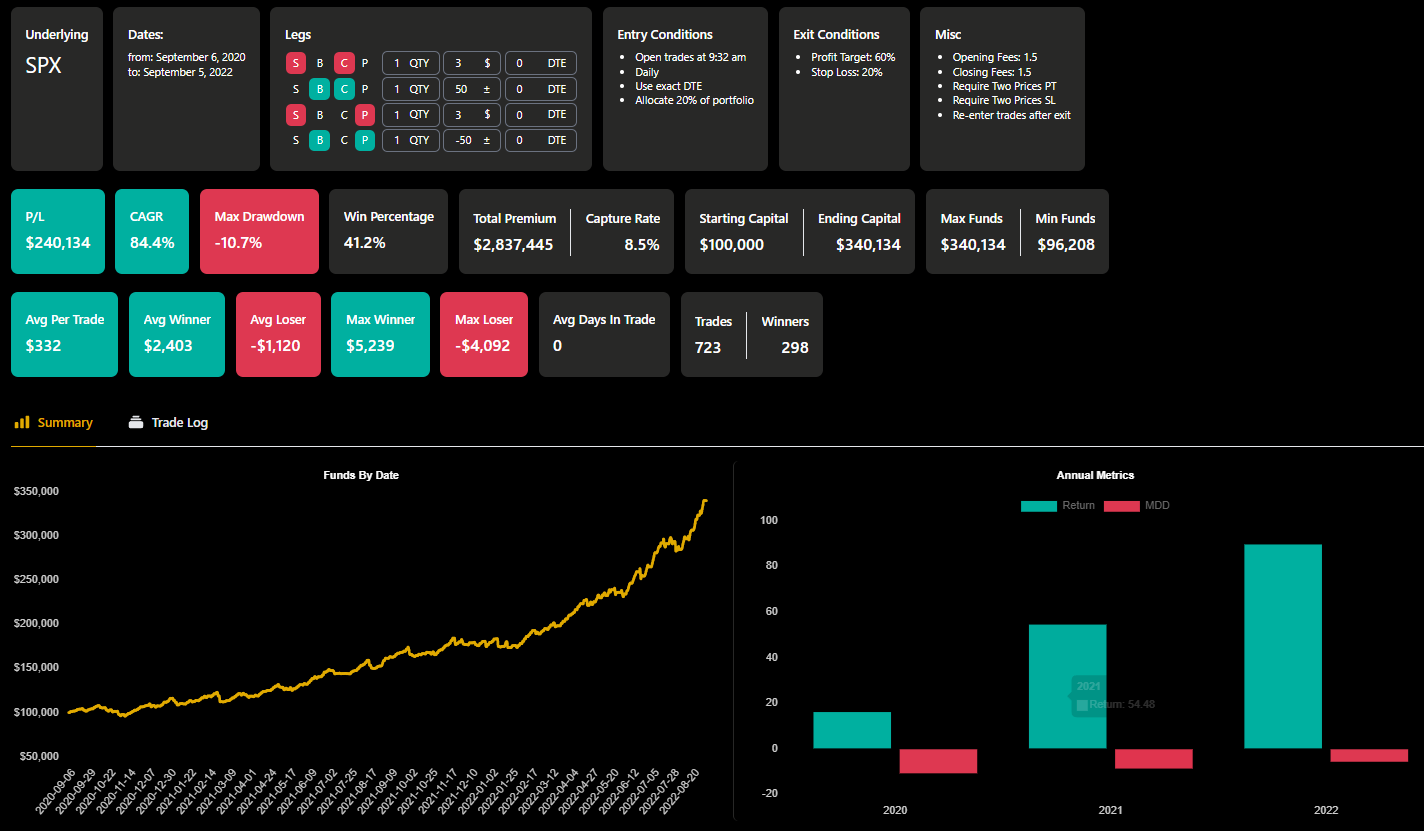

The one above is $5 each side, lets do $3.

Well $3 looks pretty neat too, with 84.4% CAGR and 10.7% max drawdown. It's quite a consistent variation compared to the $5 one.

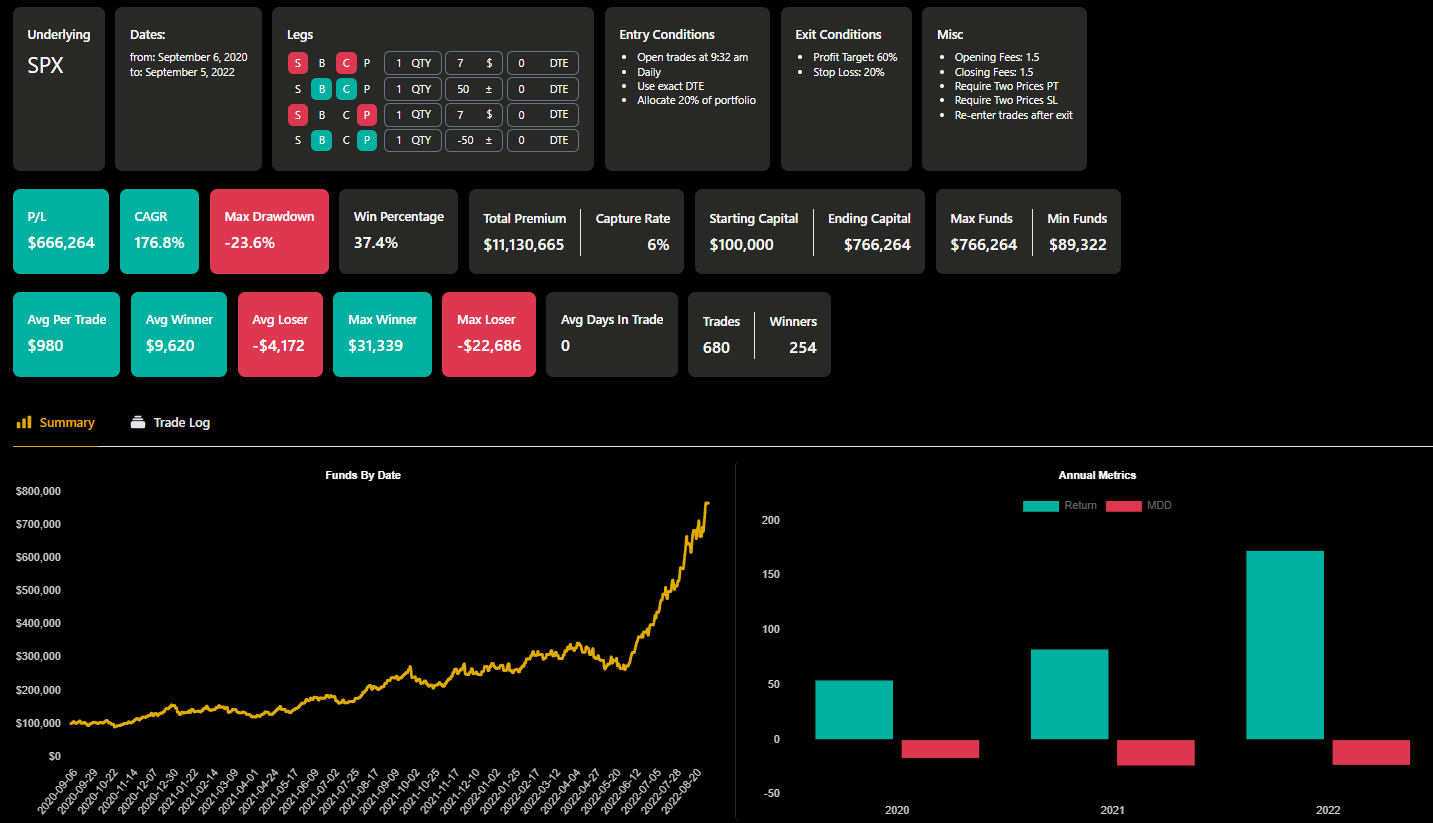

Let's do $7.

The CAGR % gets even more crazy, of course with higher max drawdown. Noting that the recent few months are performing in a pretty crazy mode. Might be a seasonal thing.

Once again I keep saying, backtest doesn't represent the future. It gives us data point to reference to find certain trends and pattern to design our strategy.

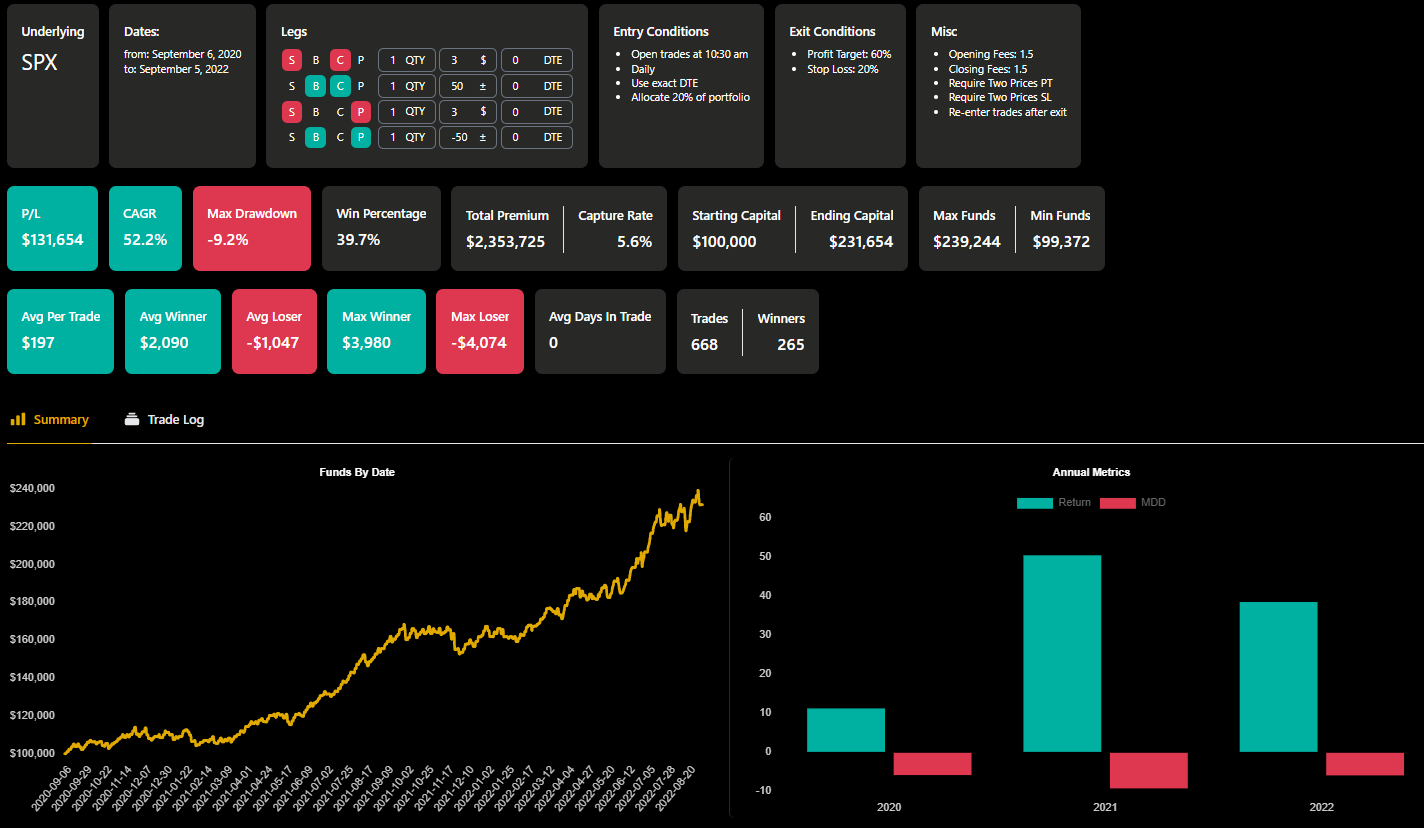

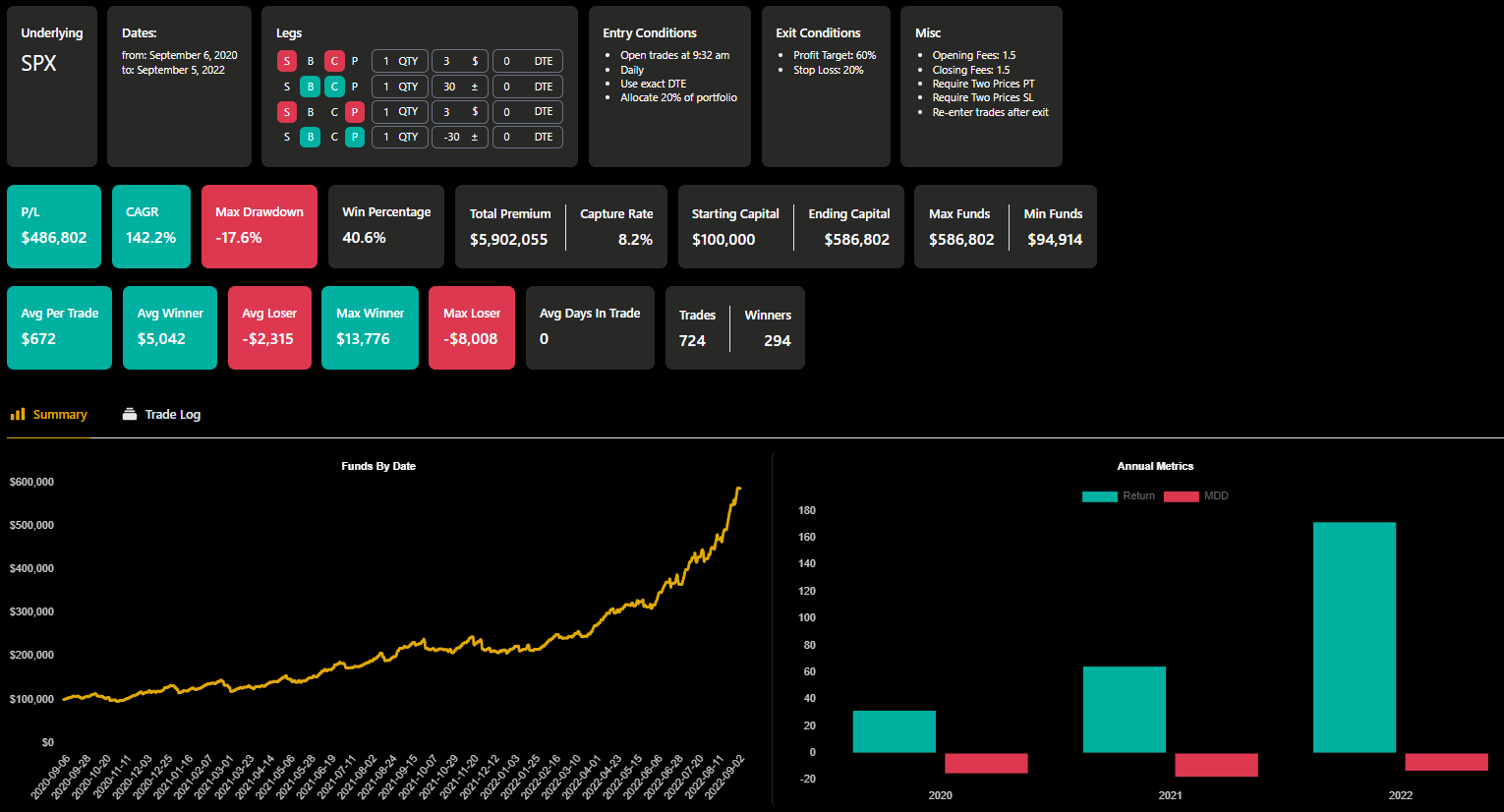

Next to tweak - lets try Timing

Among the 3 different variation above, I kinda prefer the consistent strategy. As I feel that high max drawdown is often the big factor that impact emotions. So I'll use the $3 to further tweak.

Not going to go hardcore all timings, let's do per hour.

Looks like the initial 9:32 entry has the best performance and consistent P&L curve.

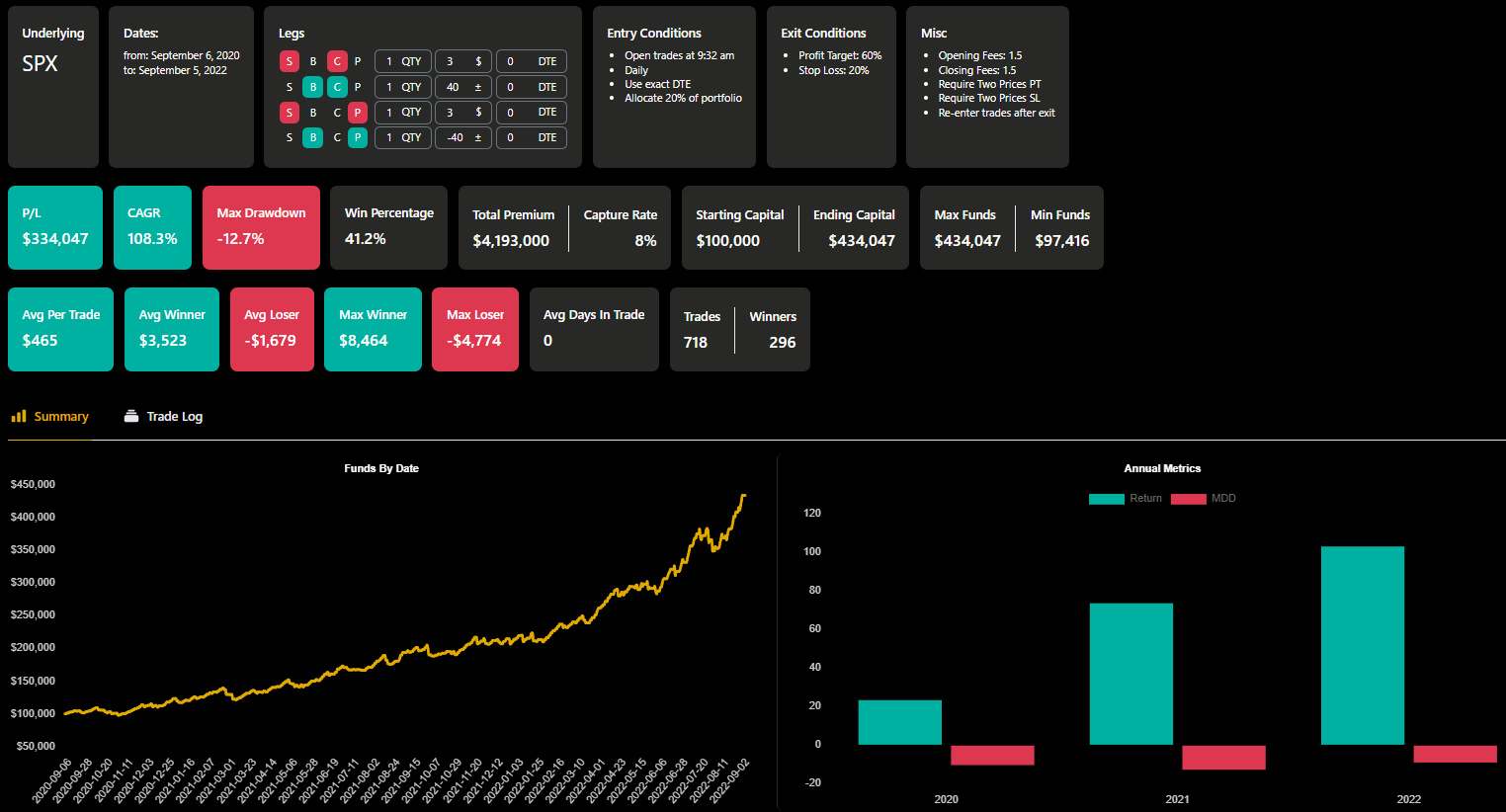

What's next? Hmm - Width

Let's continue with the best configuration so far. $3 IronCondor at 9:32.

Some quick conclusion I can take away is smaller width basically increases leverage. Not forgetting the backtest is using 20% allocation, which is compounding. I set it such that I can see drastic differences in backtest.

Smaller width increasing leverage also means higher max drawdown, which is a consistency consideration. The wider it is, the lower the drawdown. Different individual has different appetite, that's why backtest can help to design your personalise strategy.

Conclusion

This backtest was pretty adhoc, not well planned. Some idea sparked and I ran it. This post illustrate how I tweak and refine backtest on OO. If you got any ideas, please feel free to leave a comment below now that the comment feature is enabled. (It's a new feature enabled from the blog provider Ghost.io, not that I didn't want to enable it previously)

OptionOmega is quite addictive sometimes, throwing the disclaimer once again.

Member discussion